How Small Businesses Build Resilience

Strategies and tools owners turn to when facing hardship or preparing to seize new opportunities

Sustaining a small business often requires owners to pivot and adapt, like offering new products and services or adopting new technology. Although every business is different, understanding how owners change in response to challenges provides useful lessons for building resilience.

In partnership with Masters of Scale and Morning Consult, the Capital One Insights Center surveyed 1,049 small business owners in the US to better understand what strategies entrepreneurs have taken since 2020 to adapt to hardships and uncertainty. Respondents were comprised of small business owners with at least one employee and less than $20 million in total annual revenues.

We analyzed responses by length of ownership and business revenue, which revealed how business needs, strategies and expertise evolve along an owner’s journey.

A key theme that emerged was the importance of customer input, with owners reporting that they made changes to better meet customer needs, sought feedback from customers when deciding whether and how to pivot, and credit listening to customers as an aspect of having made changes effectively.

“At Capital One, we recognize how critical resilience is to a business’s ability to recover or maintain operations when adversity hits,” said David Rabkin, Head of Business Cards & Payments at Capital One. “By sharing the experiences and lessons learned from business owners that have navigated their own challenges, we hope to strengthen the capacity of other entrepreneurs to cope with stressors and seize opportunities when they arise.”

What does it mean to be resilient?

Resilience is defined as the process of adapting well in the face of adversity. While there is no unified definition for business resiliency, at a fundamental level it is a business’s ability to survive and to recover. Previous research defines small business resilience as the ability to bounce back after or adapt to adverse situations, perhaps by seizing new opportunities and swiftly implementing changes.

Many small businesses oftentimes have limited resources and bandwidth, which can sometimes undermine their ability to collaborate, innovate or be responsive to new opportunities. But they also have advantages over larger businesses that can make them more resilient, like smaller staff and less bureaucracy, which can lead to quick decision-making and faster learning cycles.

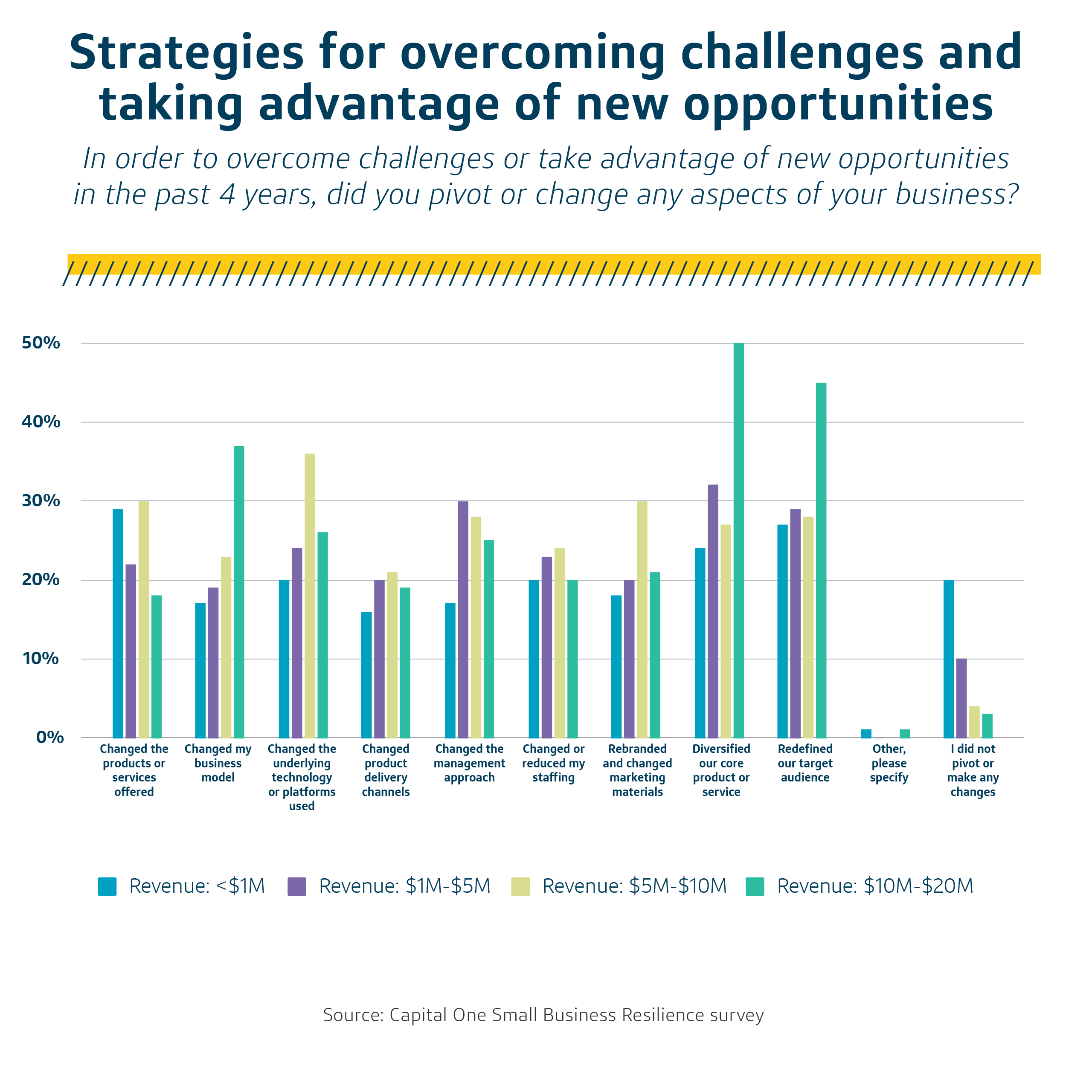

What strategies do small business owners take to weather tough times?

To overcome challenges or take advantage of new opportunities, nearly a third (31%) of small business owners said they diversified their core product or service. The same share said they redefined their target audience.

This was especially true among businesses with revenue between $10 million to $20 million, where 50% said they diversified their core product or service and 45% said they redefined their target audience (compared with 24% and 27%, respectively, among businesses with less than $1 million in revenue).

Among all respondents, about a quarter said they changed the products or services they offered, changed the underlying technology or platforms used or changed their management approach.

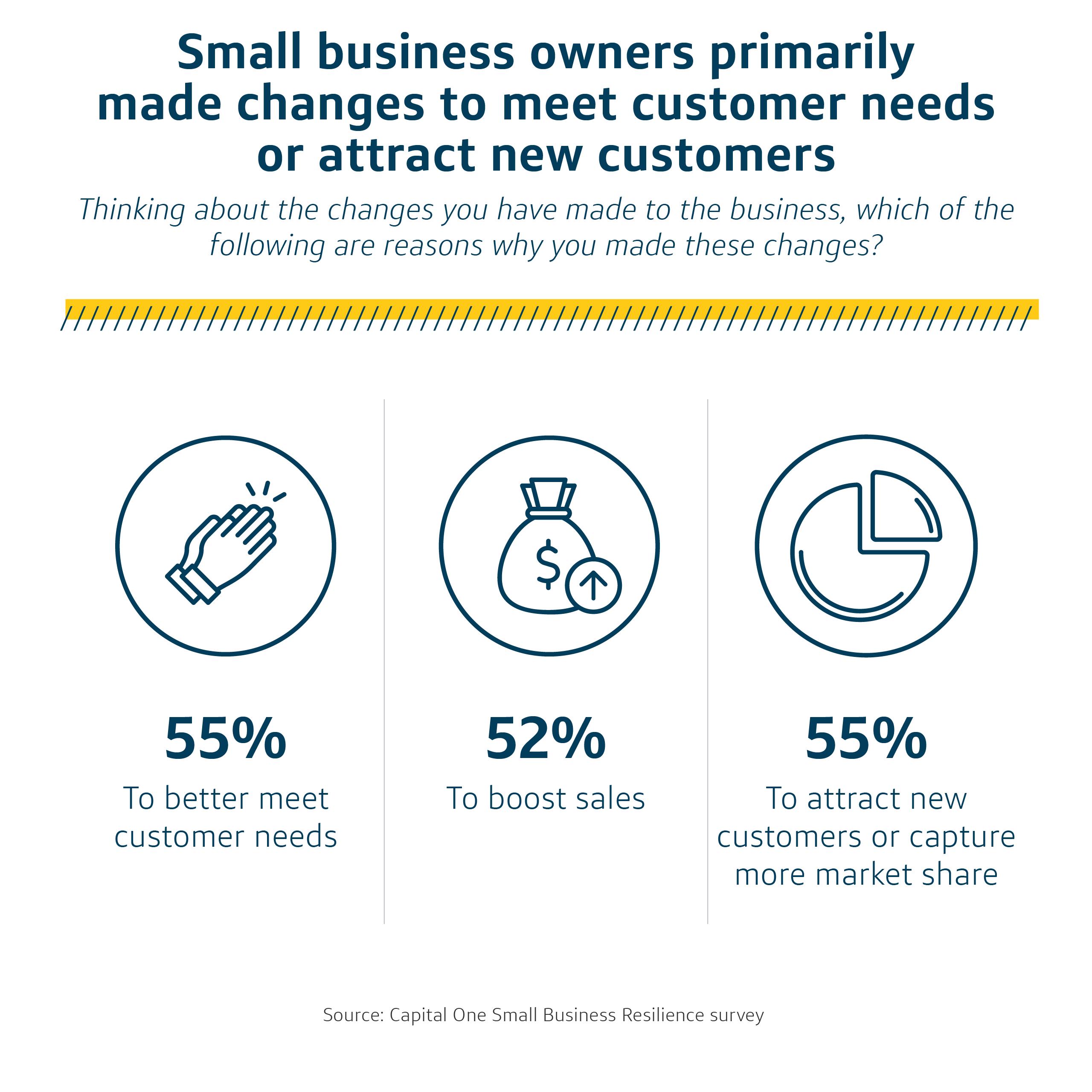

Why did owners make changes to the business?

Over half of small business owners made changes to better meet customer needs (55%), attract new customers (55%) or boost sales (52%).

How did small business owners decide how to pivot?

Across the board, regardless of company’s age or revenue, small business owners’ top resource for deciding whether and how to pivot was feedback from customers. Nearly half (49%) said they sought customer feedback, followed by 38% who sought feedback from employees.

Younger companies, and those with greater revenue, also sought guidance from their network and from Small Business Development Centers.

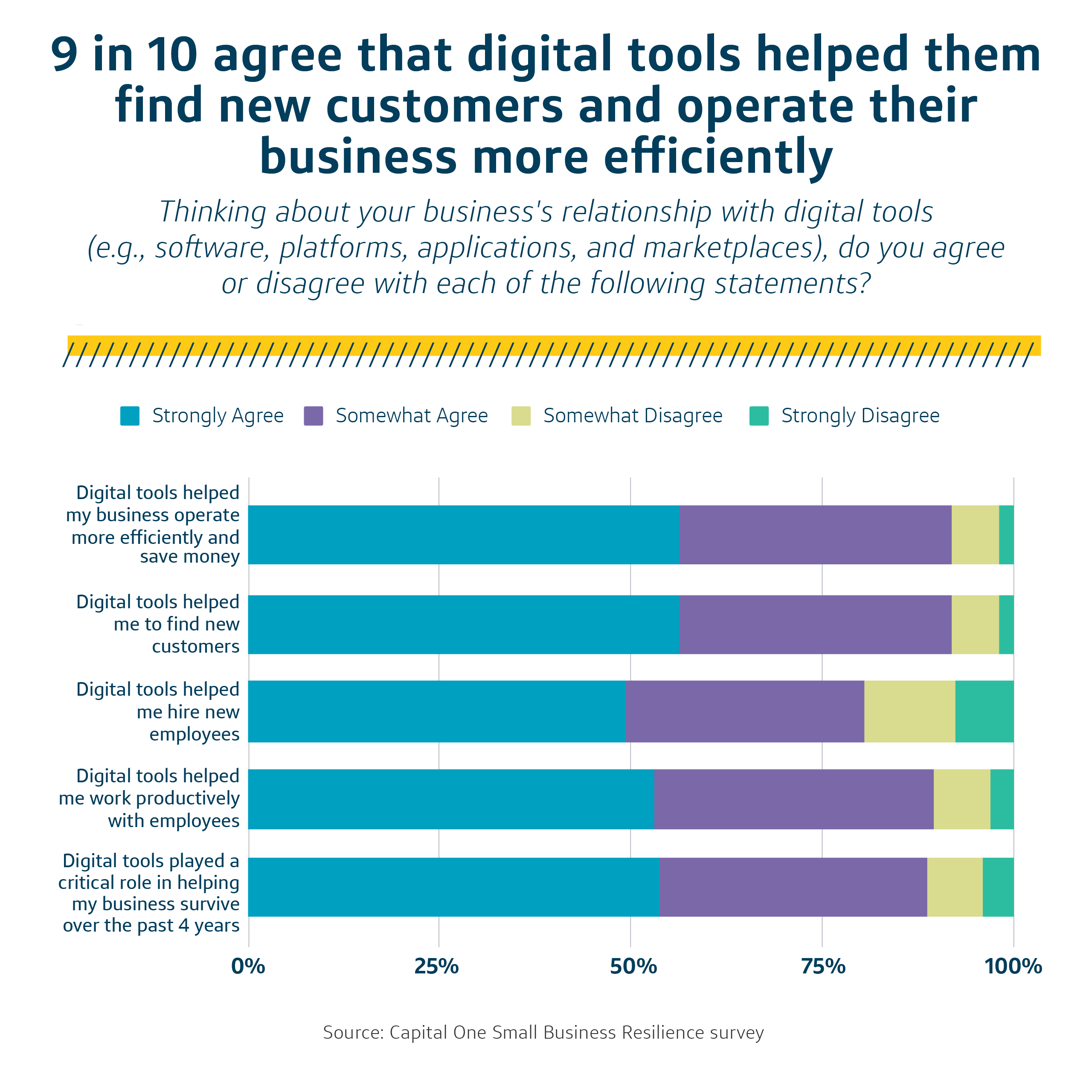

What resources did owners turn to for help?

Over half (53%) of small business owners said that listening to their customers allowed them to make changes effectively. Owners also cited low overhead costs and digital tools and technology as key factors in their ability to successfully pivot.

In fact, 90% of small business owners agreed that digital tools helped them find new customers—and finding new customers is one of the top reasons respondents made changes to their business. Owners also overwhelmingly agreed that digital tools helped them run their business more efficiently (90%) and survive over the past 4 years (86%).

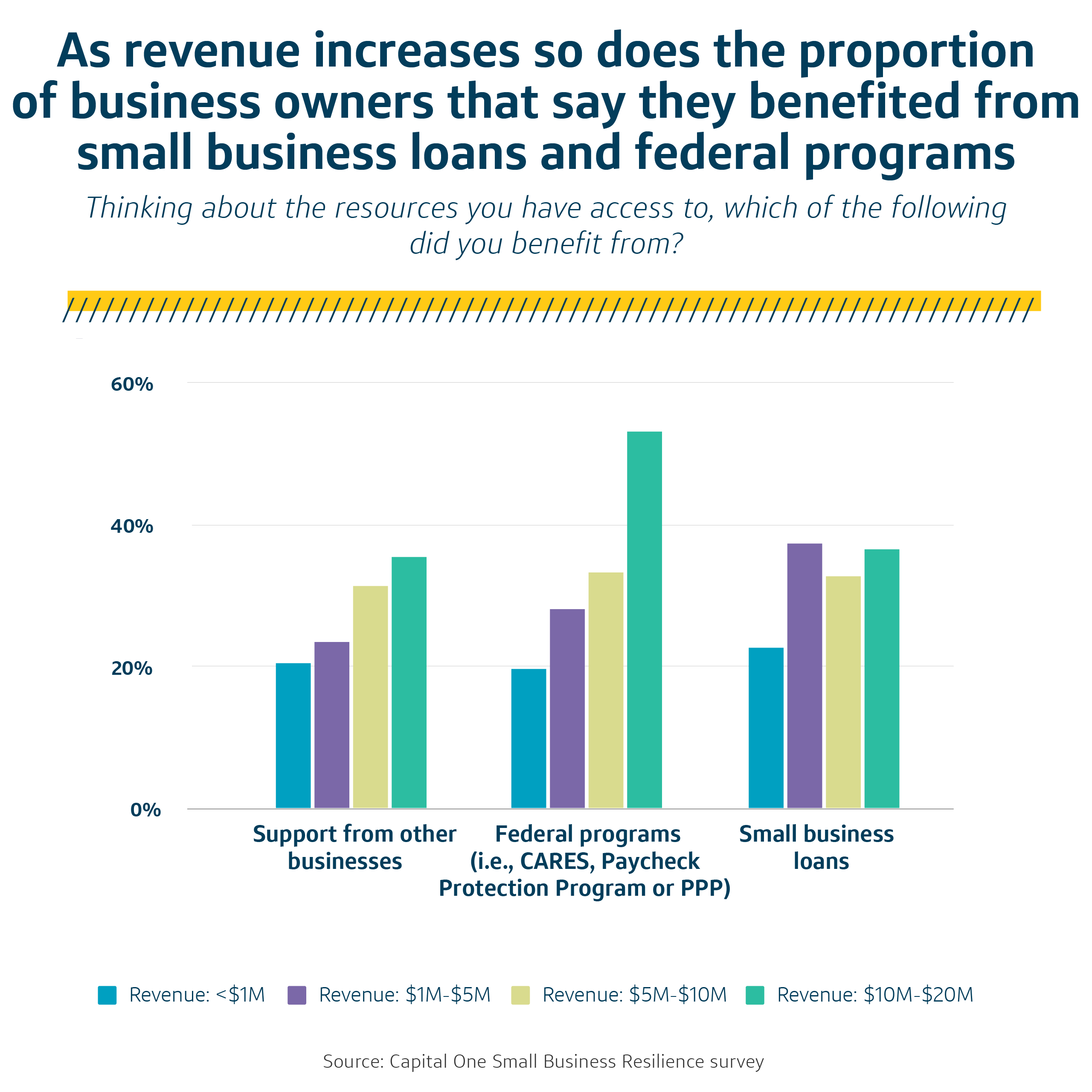

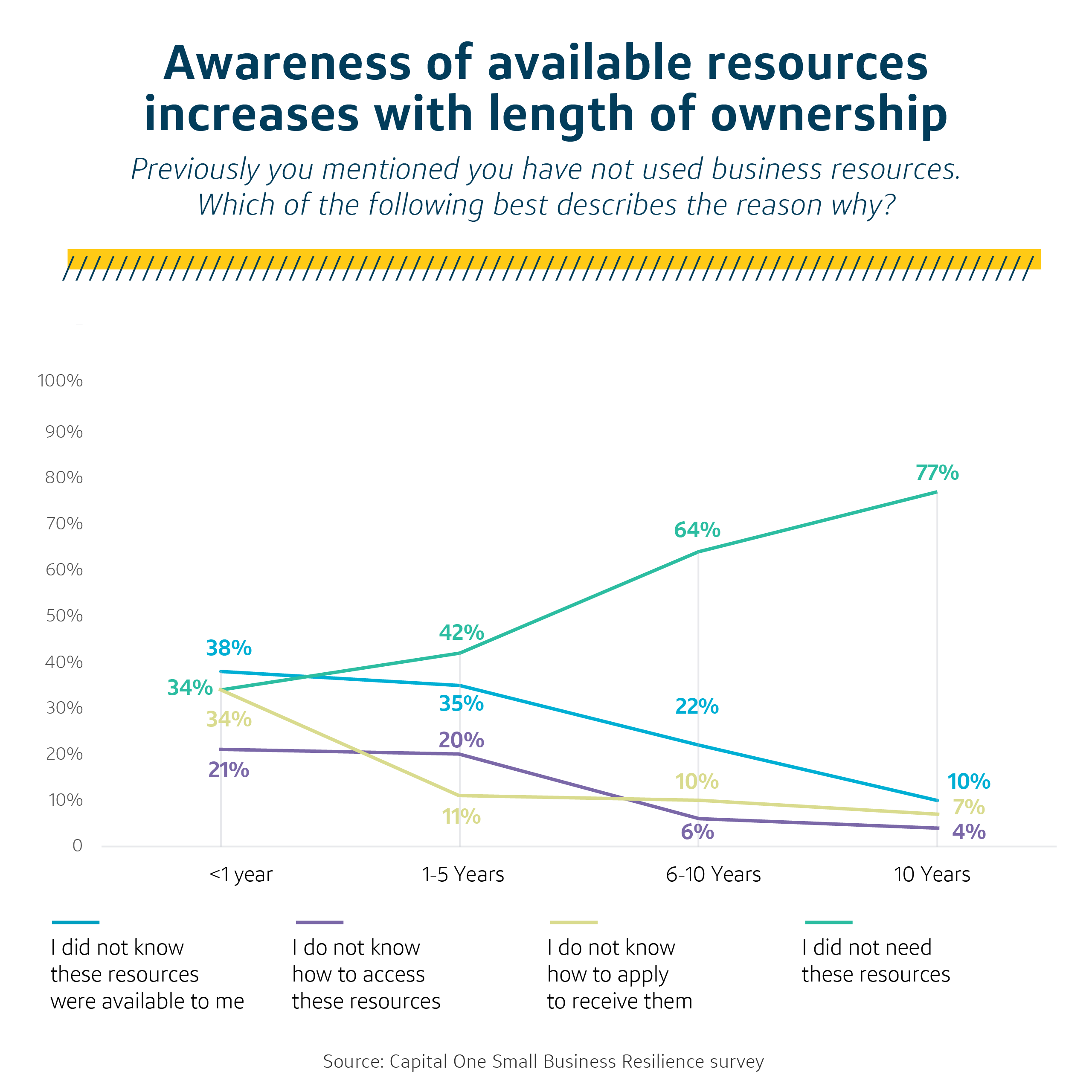

Across each resource included in the survey- support from other businesses, federal programs, or small business loans-, as revenue increased so did the proportion of business owners who said they benefited from that resource. The most used resource was in the federal programs category among business owners with revenue between $10 and $20 million.

Among owners who did not use one of these resources, younger businesses and those with lower revenue were more likely to not know that resources were available to them. We also found that more established companies and those with greater revenue were more likely to say that they did not need these resources. This finding suggests an opportunity to help small businesses grow by increasing access to public and private sector funding and programs, particularly those with revenue less than $1 million.

How do small business owners fare when it comes to their personal resilience?

Previous research highlights how important an owner’s personal and psychological resilience is to the business’s resilience. When an owner feels stress, anxiety and burnout, they may be less able to spot areas for innovation or lead through change, which can diminish the chances that their business survives.

Owning a business can take a toll, with over half (52%) of small business owners saying that their role has caused them stress over the past year and more than a third (35%) feeling mental exhaustion.

But despite feeling stressed, over 90% of owners agreed that problems can be solved, that they had an optimistic outlook and that they embodied the spirit of never giving up. Stakeholders can foster that entrepreneurial spirit by supporting small business owners at all stages of their journey.

How can stakeholders support small business resilience?

Previous Insights Center research points to the importance of a coordinated business ecosystem to provide technical assistance, network connections and access to capital—all of which is crucial to helping small businesses reach their wealth-building potential.

Smaller firms may benefit from forming communities of practice or social networks because they often face similar constraints in times of crisis. Also, because business owners said they rely on digital tools and technology, online education platforms and resources can help entrepreneurs learn from others and broaden their skills.

Methodology

Note: all data in this report is from self-reported, anonymous research of U.S. consumers broadly, not specifically from or about Capital One customers or employees.

The Capital One Small Business Resilience survey was conducted February 2-11, 2024 among a sample of 1,354 business owners with revenues of up to $50 million. The findings here consider only the 1,049 small business owners in our sample, defined as those with more than one employee and total annual revenues of less than $20 million.

The interviews were conducted online and the data were unweighted.

Results from the full survey have a margin of error of +/- 3 percentage points.

About the Capital One Insights Center

The Center combines Capital One research and partnerships to produce insights that advance socioeconomic mobility. As a nascent platform for data and dialogue, the Center strives to help changemakers create an inclusive society, build thriving communities and develop financial tools that enrich lives. The Center draws on Capital One’s deep market expertise and legacy of revolutionizing the credit system through the application of data, information and technology.

Disclaimer

This material has been prepared by the Capital One Insights Center, a non-partisan center for objective research and insights, and is provided solely for general information purposes. Unless otherwise specifically stated, any views, analysis or opinions expressed herein are solely those of the Capital One Insights Center’s staff, researchers and listed partners (if applicable) and may differ from the views and opinions expressed by Capital One Financial Corporation, other departments or divisions of Capital One Financial Corporation, or its affiliates and/or subsidiaries (Capital One). Information has been obtained from sources believed to be reliable.

The data relied on for this report are based on self-reported survey data from anonymous respondents across the U.S. Survey respondents included may or may not have relationships with any number of financial institutions and/or products. Capital One Insights Center does not know, nor is it able to determine, if any of the survey respondents have a relationship with Capital One. Certain information herein is also based on data obtained from third-party sources believed to be reliable.

Analysis and conclusions constitute the Capital One Insights Center’s judgment as of the date of this report and are subject to change without notice. Furthermore, the analysis and views will not be updated or otherwise revised to reflect information that subsequently becomes available or circumstances existing, or changes occurring, after the date of publication.

Any opinions expressed herein should not be construed as an individual recommendation for any particular customer or client and is not intended as advice or recommendations of particular securities, financial instruments, market conditions or strategies. Capital One Financial Corporation and its affiliates and/or subsidiaries may issue reports or have opinions that are inconsistent with, and reach different conclusions from, this report.